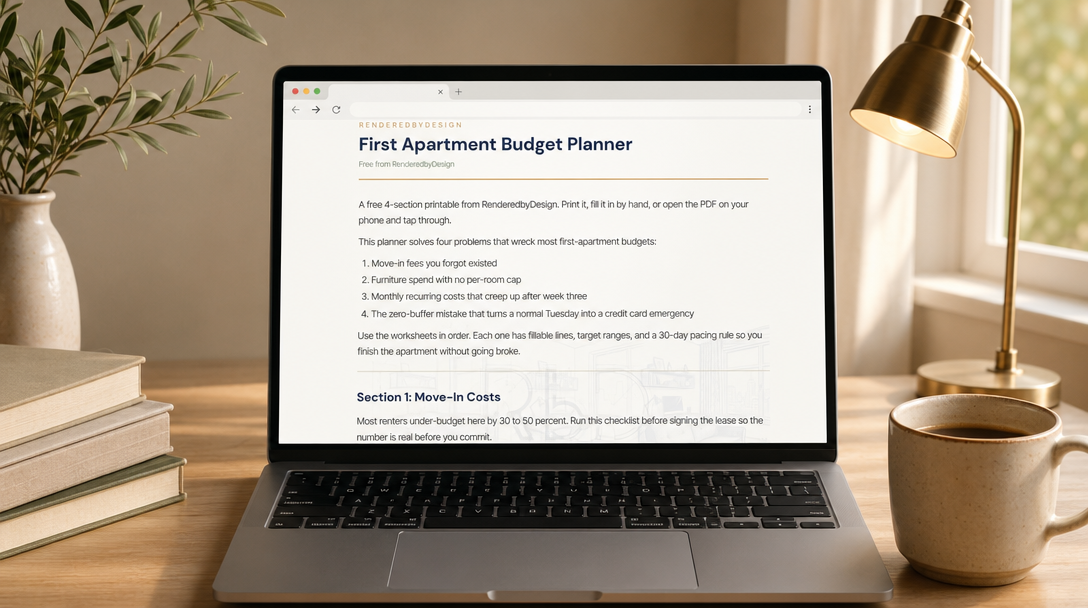

Table of Contents

The single most-validated budgeting narrative among renters is not a method. It is a habit. One renter put it this way: "I've always been terrible with money. Living paycheck to paycheck despite making decent income ($68K). Last January, after another month of wondering where my money went, I decided to track EVERY single transaction for a full year." That sentence resonates more than any method-specific advice. The audience does not need a system. The audience needs visibility.

So this planner is built around that insight. The first worksheet is not a method. It is a "track every penny" log: 30 days of every transaction, copied from a phone or bank app at the end of each day. Methods (50/30/20, zero-based, envelope) come second, after one month of real numbers is on the page. The sample $50K NYC first-apartment budget on the facing page is the example to measure against.

Why "track every penny" beats every method.

Here's the catch with method-first budgets: they assume the numbers are already known. Most first-apartment renters have a vague sense of "rent eats half my paycheck" and "takeout is probably too high," but no actual number for either. Picking 50/30/20 before one month of data lands is choosing a recipe before checking what is in the fridge.

The 30-day tracking exercise.

Every transaction. Including the $4 coffee. Including the $0.99 in-app purchase. Including the $14 grocery delivery fee. The point is not judgment. The point is the bar chart that emerges at end of month 1. Most people are surprised by exactly two categories: how much went to "small" purchases (coffees, app subs, in-app buys, parking) and how much disappeared into recurring subscriptions they forgot they had.

The two surprises that show up almost universally.

Surprise one: subscriptions. One renter described the audit experience: "I cancelled or downgraded almost all of my subscriptions." Most renters carry 6 to 14 active subscriptions and use 3 to 5. The annual cost of unused subscriptions averages $300 to $700. Surprise two: convenience fees. Grocery delivery surcharges, ATM fees, overdraft fees, takeout app fees, and credit card cash-advance fees compound to $40 to $90 per month for renters who do not track them.

How to fill out the planner in 15 minutes.

Here's how this actually works. Grab the planner, the last paystub, and the last 30 days of bank and credit-card statements. The whole thing takes 15 minutes, no spreadsheet required. Do not aim for perfect categorization on the first pass. Aim for visibility, the number that shows what is coming in and what is going out before any optimization starts.

Step 1: write down your monthly take-home pay.

Take-home, not gross. After taxes, after retirement contributions, after insurance, after any pre-tax deductions. The number that hits your checking account on payday. If you are paid bi-weekly, multiply one paycheck by 2.17 (not 2). If you are paid hourly, use the average of the last 8 weeks.

Step 2: list fixed needs.

Rent. Utilities. Internet. Phone. Insurance (renters, health, auto). Minimum debt payments. Transit pass or car loan plus gas. Groceries (use the last 30 days as the baseline). The "fixed needs" line should not exceed 50 percent of take-home for the budget to function. If it does, see the "When rent and food eat 100 percent" section below.

Step 3: list variable wants.

Dining out. Coffee. Subscriptions. Entertainment. Hobbies. Travel. Beauty. Clothing. This category is where most renters find the leak. The honest version of this line is usually 30 to 40 percent higher than the renter's first guess.

Step 4: write the savings target.

20 percent of take-home is the textbook target. 5 percent is the realistic floor for first-year renters. Whatever the number is, write it down before you see how much is left, not after. Savings is a fixed need, not a leftover.

The 50/30/20 method.

Here's the math: 50 percent of take-home covers needs, 30 percent covers wants, 20 percent goes to savings and extra debt payment. It's the simplest method to start with, and the one most likely to survive the first year intact.

What counts as a need.

Rent, utilities, groceries (the basic version, not the gourmet version), transportation, insurance, minimum debt payments. The test: would you stop paying for it if you lost your job? If yes, it is a want.

What counts as a want.

Dining out, takeout, coffee shops, subscriptions, entertainment, hobbies, travel, gym, beauty, clothing beyond replacement. None of these are bad. The 30 percent ceiling is what makes the rest of the budget hold.

When 50/30/20 breaks.

High-rent cities (NYC, SF, LA, Boston) routinely push the rent line above 40 percent of take-home, which means needs alone exceed the 50 percent target. The solution is not to give up on the method. The solution is to flex it: 60/25/15 is more realistic for first-year renters in HCOL markets, with the savings line restored to 20 percent in year two when income grows.

The zero-based method.

Here's the rule: every dollar gets a job before the month starts. Income minus expenses minus savings minus debt equals exactly zero. Nothing is left "unassigned." The advantage is intentionality. Every dollar in the account is already pointed at a category. The trade-off is up-front effort. Zero-based requires more setup than 50/30/20, but renters who run it report the highest sense of control of any method.

How to set up zero-based in one sitting.

List every category you spend on. List the dollar amount each category needs in a typical month. The total should equal your take-home pay exactly. If income is higher, assign the extra to "savings" or "extra debt payment." If income is lower, cut wants until the math works. The categories you assign are the categories you spend in. Anything not on the list does not get bought without a deliberate re-allocation.

The YNAB rule.

YNAB (You Need A Budget) is the most popular zero-based budgeting app. Opinions are split on the price increase, but YNAB's "give every dollar a job" methodology is the strongest implementation. The free alternative: a Google Sheet with the same setup, updated weekly.

The envelope (cash) system.

Old method, still works. Here's the setup: cash for variable categories (groceries, dining, entertainment, hobby spend), allocated at the start of the month into physical or digital "envelopes." When the envelope is empty, the category is closed for the month. The hard stop forces a decision before the swipe, not after.

The digital version.

One renter describes the modernized version: "I consciously spend by transferring the exact amount needed each purchase from my monthly budget account to my $0 balance spending account. Annoying? You bet. Have I kept my budget 4 months straight? You bet." Two checking accounts. The "main" account holds your income. The "spending" account stays at $0. You move money to the spending account each time you spend. The transfer creates a 5-second pause that kills 30 percent of impulse purchases.

When envelope wins.

Envelope is the strongest method for renters who say "I cannot stop overspending on dining out" or "I always blow the grocery budget." The hard cap forces the decision before the credit card swipe. Envelope is the weakest method for renters with strong digital-only spending (online subscriptions, app purchases) since most of those bypass the cash envelope entirely.

A real $50K NYC first-apartment budget, line by line.

Here is why concrete examples beat blank templates. The budgeting posts that resonate most widely are the ones that share actual numbers, not hypothetical categories. Below is the sample budget that ships filled-out on Page 1 of the PDF lead-magnet.

The numbers.

Salary: $50,000. NYC outer-borough one-bedroom. Take-home pay (after federal, state, NYC tax, plus 401k 5 percent and health insurance): roughly $3,200 per month. Below is one realistic allocation:

- Rent: $1,400 (room in shared apt or studio in deep outer borough)

- Utilities + internet: $120

- Phone: $40

- Groceries: $400

- Transportation (MTA pass): $132

- Renters insurance: $15

- Household supplies: $40

- Total fixed needs: $2,147 (67 percent of take-home, above the 50/30/20 ideal)

- Dining out + takeout: $300

- Subscriptions (Netflix, Spotify, gym): $50

- Entertainment + hobbies: $150

- Total wants: $500 (16 percent of take-home)

- Emergency fund: $250

- Apartment build-out fund: $200 (couch, dresser, art over the year)

- Roth IRA: $100

- Total savings + build-out: $550 (17 percent of take-home)

Total: $3,197 of $3,200 take-home. The math works. Wants are tight. The build-out fund is intentionally separated so the "I need a rug right now" impulse hits a real $200/month line, not the dining-out budget.

Build the same line-by-line for your city.

The companion first apartment budget planner walks through three salary-x-city variants ($50K NYC, $65K Chicago, $80K Austin). Pair it with this monthly budget planner: that one shows what a budget looks like for someone like you, this one is the tool you fill out for yourself.

Common budget mistakes (and how to catch them).

1. Budgeting gross instead of net.

The single most common first-budget mistake. Here's how it plays out: budgeting $4,200/month gross when only $3,200 hits the account leaves the renter $1,000 short by month-end. Use take-home pay only, every time.

2. Rounding everything to whole dollars.

The 99-cent rounding error compounds. Track to the dollar, not the round number. Renters who say "I always under-budgeted" consistently trace the gap to rounding down.

3. Once-a-month review.

By the time month-end check-in arrives, the overspend has already happened. Here's the better cadence: reconcile weekly, 5 minutes on Sunday night, not monthly. Weekly catches drift while there's still time to course-correct.

4. Forgetting irregular bills.

Annual subscription renewals. Quarterly insurance. Twice-yearly registration. Birthday gifts. Holiday spending. None of these hit a typical month, then they all hit at once. Use a "sinking fund" line to set aside one-twelfth of each annual bill every month.

5. Treating the budget as restriction, not visibility.

The strongest reframe comes from the renter who said tracking "completely changed my relationship with money." A budget tells you what your money is doing. It does not tell you what you cannot have. Renters who frame the budget as visibility outlast renters who frame it as restriction.

When rent and food eat 100 percent of your paycheck.

Here is the most honest critique of generic budget advice: "Every financial advice article says build an emergency fund. Save three to six months of expenses. Put away money every paycheck. Where? Where does the savings come from? Rent plus food plus utilities equals 100 percent of my income. Sometimes more. There is no surplus. There is no extra money to put away."

If that paragraph describes you, the standard budget advice does not apply. The planner has a separate worksheet for this case. Three actions in priority order:

Action 1: audit subscriptions ruthlessly.

One renter's breakthrough: "I cancelled or downgraded almost all of my subscriptions." The single fastest $50 to $200 you will find in your monthly budget is sitting in unused subscriptions. Open every recurring charge in your bank statement. If you have not used it in 30 days, cancel it.

Action 2: shift the grocery budget to staples.

Rice, beans, eggs, oats, frozen vegetables, canned tomatoes, peanut butter, cabbage, onions. Together, these can feed one person on $30 per week. Renters living on tight budgets consistently share how to make $500 a month in food work for one person. The cookbook is "Good and Cheap" by Leanne Brown (free PDF online, written specifically for SNAP budgets).

Action 3: add income, not just subtract spending.

When the budget is already at the floor, the next dollar has to come from a new income source, not a smaller expense. A $200/month side income (delivery, freelance, weekend retail, language tutoring, dog walking) is the difference between sinking and stable for renters at the bottom of the budget. Renters who have been there confirm it: small income additions compound faster than expense cuts when the budget is already at the floor.

Pair the planner with the cluster.

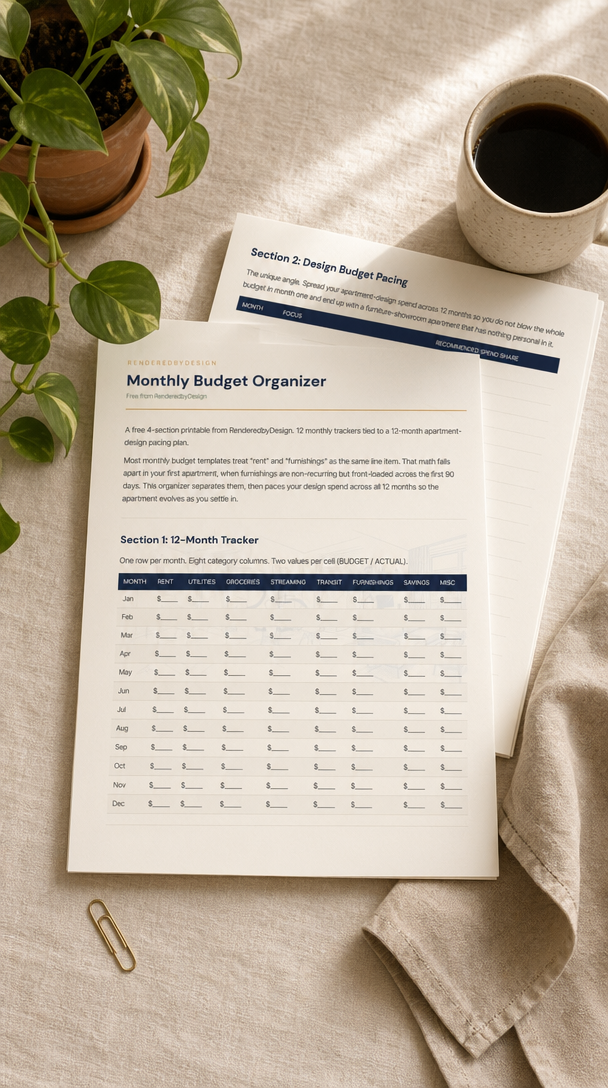

The budget is the spine of every other apartment decision. Pair this planner with the first apartment checklist for what to buy across Day One, Week One, Month One, and the first apartment essentials shopping list for the priced version with retailer comparisons. The apartment cleaning checklist covers the household-supplies line item with apartment-safe products only. The lead-magnet PDF: RbD-Monthly-Budget-Organizer.pdf.

Frequently asked

What is the easiest budget method for beginners?

Track every penny for 30 days before picking a method. The single most-validated budgeting narrative among renters is "I tracked every penny I spent for a year and it completely changed my relationship with money." Method comes after data. Once you have one month of real numbers, the 50/30/20 method is the easiest entry point: 50 percent of take-home for needs, 30 percent for wants, 20 percent for savings and debt.

What is the 50/30/20 budget method?

Take your monthly take-home pay (after taxes). 50 percent goes to needs (rent, utilities, groceries, transportation, insurance, minimum debt payments). 30 percent goes to wants (dining, entertainment, subscriptions, hobbies, travel). 20 percent goes to savings and extra debt payment. The planner has the math built in. For a $4,000 monthly take-home: $2,000 needs, $1,200 wants, $800 savings.

What is zero-based budgeting?

Every dollar you earn gets a job before the month starts. Income minus expenses minus savings minus debt equals zero. Nothing is left "unassigned" to drift into impulse spending. The advantage: every dollar is intentional. The disadvantage: it requires more effort up front. Zero-based shines for renters who say "I make decent money but I have no idea where it goes" (a common refrain among renters earning decent money).

What if my rent and food eat 100 percent of my paycheck?

The question "where does the savings come from?" speaks for a real audience that generic budget advice ignores. Three actions when rent plus food equals 100 percent: first, audit subscriptions ruthlessly (renters routinely find $200 a month in unused subscriptions when they audit). Second, every grocery dollar moves to lowest-cost-per-calorie staples (rice, beans, eggs, oats, frozen vegetables). Third, add income, not subtract spending. A $200/month side income can be the difference between sinking and stable. The planner has a separate worksheet for this case.

How do I track my spending without an app?

Three methods work. Method one: pen and paper, every transaction at end of day, reconciled weekly. Method two: a simple spreadsheet you fill out daily (literally one row per transaction). Method three: the $0 spending account trick: keep a separate checking account at $0 balance and transfer the exact amount you need from your main account each time you spend. The transfer creates a forced pause between you and the purchase.

Should I use a budgeting app like YNAB, Mint, or Rocket Money?

Apps track day-to-day. The planner sets the per-month target and the multi-month pacing. Use both. Mint shut down in 2024, so the live alternatives are YNAB (paid, the gold standard for zero-based budgeting), Copilot (paid, iOS-friendly), and Monarch Money (paid, post-Mint). Free apps tend to upsell aggressively. Opinions are split on YNAB's price increase, but it remains the most thorough tool available.

What does a real first-apartment budget look like?

For a $50K salary in a mid-cost US city: take-home roughly $3,200/month after taxes and pre-tax deductions. Rent $1,200, utilities and internet $150, groceries $400, transportation $200, phone $50, household supplies $40, total fixed needs ~$2,040. That leaves $1,160 for wants and savings. A reasonable split: $400 to dining, entertainment, subscriptions, $300 to savings and emergency fund, $300 to extra debt payment, $160 to first-apartment build-out. The companion first apartment budget planner walks through three salary-x-city variants.

Is the monthly budget planner really free?

Yes. The PDF arrives by email in under five minutes. No credit card. The planner ships with a fully-filled-out sample $50K NYC first-apartment budget on one page and a blank version on the facing page. Direct PDF: RbD-Monthly-Budget-Organizer.pdf.

Get the monthly budget planner free

Track every penny worksheet + 50/30/20 + zero-based + envelope methods + a fully-filled-out sample $50K NYC first-apartment budget. Sent to your inbox in under five minutes. Direct PDF: RbD-Monthly-Budget-Organizer.pdf.

Send me the planner