Table of Contents

Most first-time renters under-budget by 30 to 50 percent. They think about rent and forget about everything else.

Why most first-apartment budgets fail.

- Hidden fees

- No per-room cap

- Untracked recurring

- No buffer

The four sections of the planner map directly to these failures.

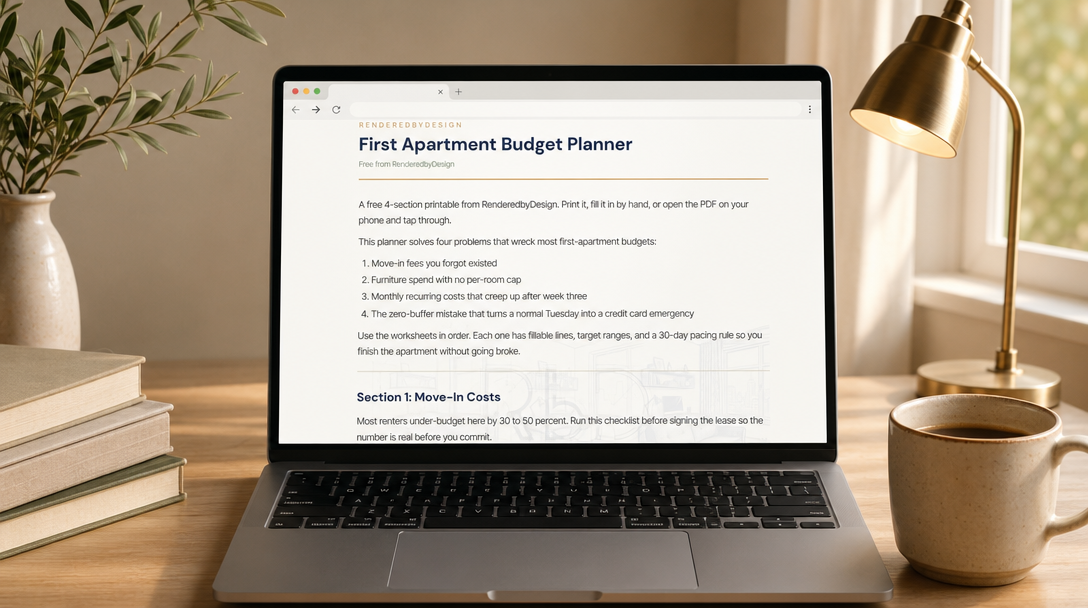

Section 1. Move-In Costs

Most renters under-budget here by 30 to 50 percent. Run this checklist before signing the lease so the number is real before you commit. The line item that sinks the most first-apartment budgets is utility security deposits when you have no payment history with the providers, often $50 to $300 per company.

Section 2. Furniture Budget by Room

Allocate your full furniture spend across rooms before buying anything. The rule we use in our renders is 6 to 10 percent of pre-tax annual income, split by room priority. Living 40 percent, bedroom 30 percent, kitchen 15 percent, office 10 percent, bath 5 percent. Cap each room first so the sofa does not eat 60 percent of the budget and leave the bedroom with $200.

Section 3. Monthly Recurring Costs

Estimate, track, audit. Run the recurring sheet for the first three months in a row. The leak that catches everyone: streaming subscriptions stack from 2 services to 5 by month 3, internet auto-upgrades when you accept the higher-tier 'free trial', and groceries balloon when you stop meal-planning after the move chaos. Target rent at 30 percent or less of net pay. If you are above 35 percent, the rest of the budget gets hard fast.

Section 4. Emergency Buffer + 30-Day Rule

Two rules that protect every first apartment. The buffer: hold one full month of rent + utilities in a separate account before you start buying decor. If you do not have it yet, slow the furniture spend until you do. Decor is reversible. A missed rent payment is not. The 30-day rule: for any non-essential purchase over $50, write the item on the planner with the date you first wanted it. Wait 30 days. Most impulse buys do not survive the wait, and the ones that do tend to be the keepers.

The bare minimum: what $1,500 to $3,000 actually gets you.

The four sections above assume a $3,500 to $7,000 budget. Not everyone has that. One creator moved from Atlanta to Portland with no savings, no job, and no apartment lined up. The strategy: a $3,000 personal loan allocated strictly to essentials. "I took out a $3,000 personal loan and I made sure to allocate that money only for things that I absolutely needed." Groceries, toiletries, a room deposit. Nothing discretionary.

The housing ladder.

When you cannot sign a lease on day one, there is a progressive cost-reduction path that gets cheaper each step: Airbnb for the first week (roughly $500), hostel for weeks two through four (roughly $600), then a room for rent once you have income (roughly $500 to $800 per month). Each step costs less than the one before, and each buys time to stabilize. "Securing a room for rent first would be the smartest way to go" if you can only do one thing before you arrive.

Take any job first.

Warehouse work, food service, retail, delivery. The advice is direct: "You're going to have to do the jobs at first that you don't want to do so that you can set yourself up to get the job that you want to have later on." Income stability enables everything else. The job you want comes after the job you need.

Apartment maintenance and leasing agent roles often pay better than food service and sometimes include housing discounts. If you are moving into a rental market, the buildings themselves are hiring. This tip came from a commenter and drew 86 likes, making it the highest-engagement practical advice in the financial category across all 16 videos.

Priority order when you can only do one thing.

Lock down housing before the job. Jobs are easier to find locally than remotely. A room for rent with a week of lead time beats a signed offer letter with nowhere to sleep. The budget at this tier is not about optimization. It is about sequencing: housing first, income second, stability third, everything else later.

Need the full financial breakdown for your city, including real rents, salary tiers, and neighborhood-by-neighborhood cost comparisons? The Move Guide for your city covers it.

Our pick.

If you only do one section before signing the lease: Section 1. Most renters who run hidden-fee math before signing avoid the credit-card scramble in week three. The rest of the planner can wait until you have keys.

Frequently asked

What does this printable cost?

Nothing. Free PDF, sent to your inbox in under five minutes. No credit card.

I am moving in two weeks. Is it too late to start?

Not at all. Run Section 1 (move-in costs) before you cut the deposit check. Skip ahead to Section 4 (buffer rule) before you start ordering furniture. Sections 2 and 3 can fill in across the first 30 days after move-in.

Does this work for couples or roommates splitting costs?

Yes. The split-cost worksheet in Section 1 has columns for two or three names with auto-totaling lines. Roommate friction usually traces back to one person tracking and one person assuming. The shared sheet ends that.

How is this different from a budgeting app like YNAB or Mint?

Apps track. Planners plan. The two work together: this planner builds the number before money moves; an app tracks against it after. Most renters need both.

What format is the planner?

PDF, 7 pages, US letter. Print it or fill it in on phone or tablet. Print version uses gold-bordered checkboxes and fillable lines in the brand pen-ink layout.

Will I get spammed?

No. You will get the planner plus three short follow-up emails over two weeks (delivery, usage tip, feedback survey). Unsubscribe anytime.

Get the planner free

4 sections. 7 pages. Every move-in dollar, every monthly leak, every furniture cap. Sent to your inbox in under five minutes.

Send me the planner